Table of contents

Please note that the information contained in this article is limited in scope and is only intended as a high-level overview of the topics discussed. The information is current as of the publication date only, and the laws (and associated agency and/or judicial interpretations) on the topics discussed could change at any point in the future. Block, Inc. (including its affiliates, subsidiaries, employees, officers, directors, attorneys, and tax advisors) undertakes no obligation to update this article for future changes in the law. In addition, laws vary by jurisdiction, and this article does not attempt to address all jurisdictions.

Managing finances can be stressful. The good news is there are tools to make maintaining your business less taxing. As a small-business owner, one of the best and easiest tools you can use is your bank statement. This article is a deep dive into bank statements and how you can use them to manage your business better.

What is a bank statement?

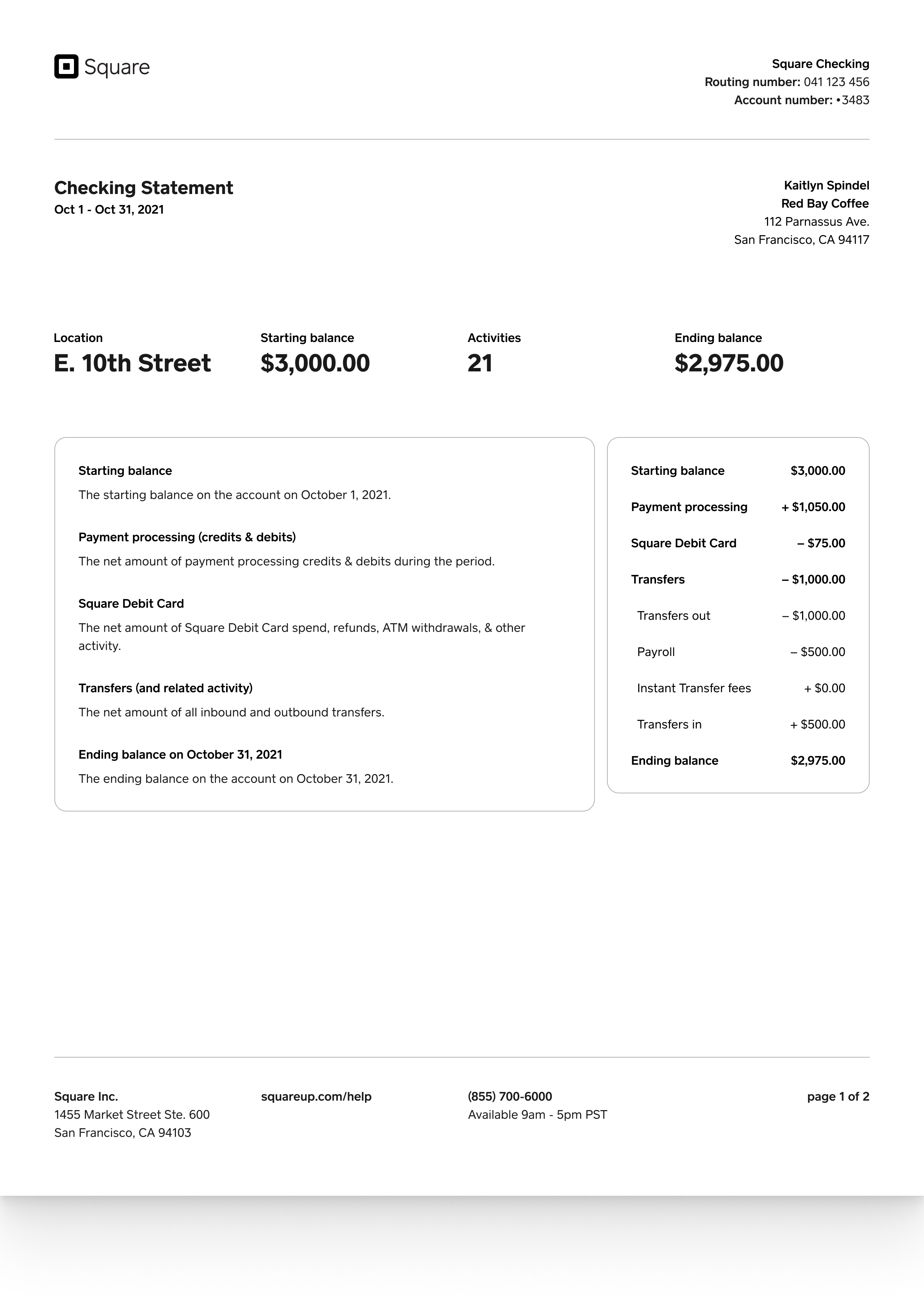

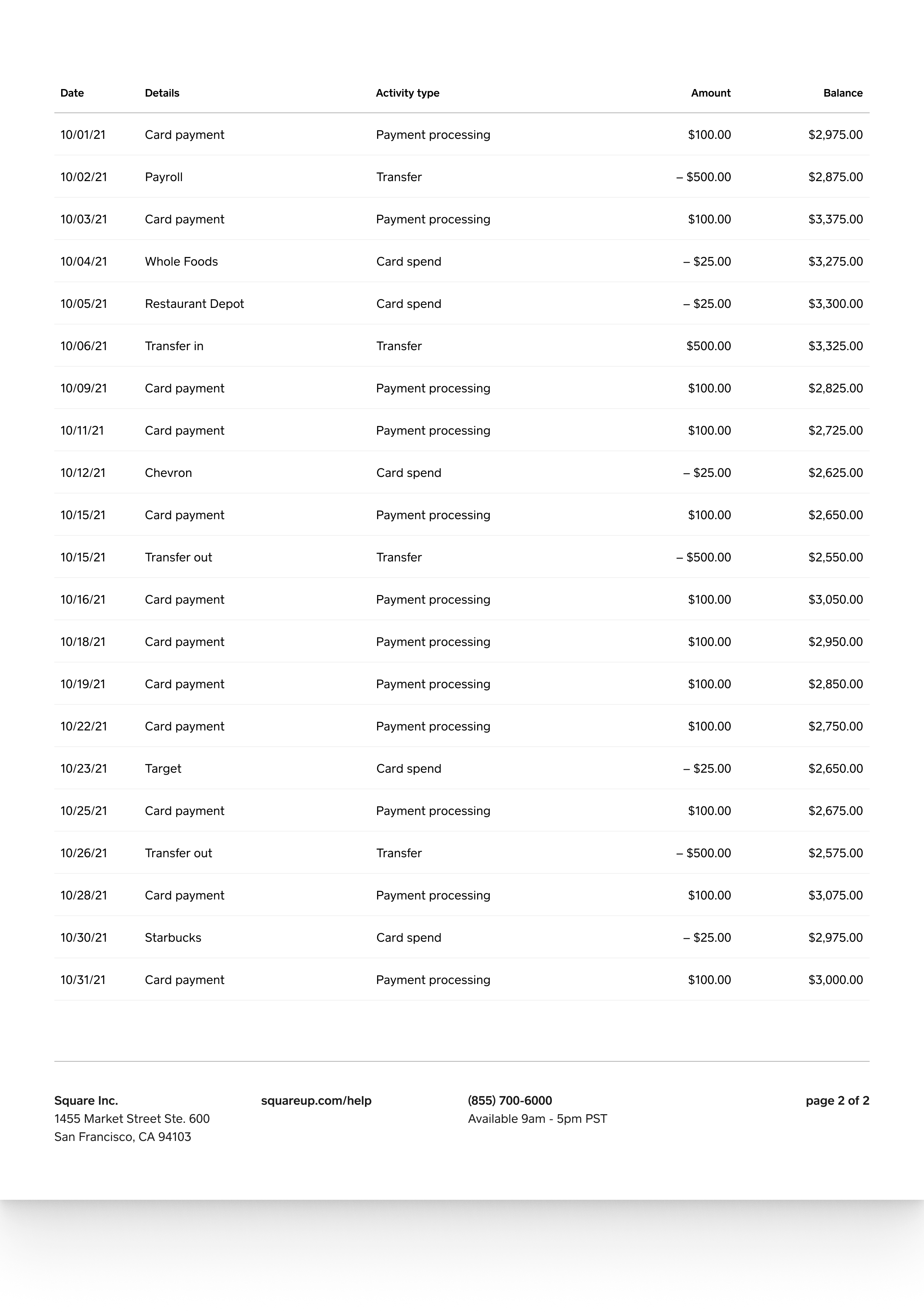

A bank statement is a document that summarizes the transactions of a bank account during a period of time, typically one month. Bank statements can come from a checking or a savings bank account, an investment account, and credit card records. There are several reasons why businesses may want to hold on to these documents. Here is a bank statement sample showing the details it typically includes:

- Information about the bank itself, including contact information

- Account details, such as your name, bank account number, address, and other personal information

- A summary of transactions, including deposits and withdrawals with a beginning and an ending balance

- The period of time summarized in the statement

Bank statements demonstrate business activity at a glance, which you can use to find any discrepancy should one arise.

The importance of reviewing bank statements regularly

As a business owner it’s important that you review your bank statements regularly. It can help you track expenses accurately, ensuring that your financial records align with your actual spending. It can help you monitor and stay within budget. It can help you identify errors, such as duplicate or incorrect charges, so you can address them with your bank or charging vendor. Lastly, it can help you address unusual or unauthorized activity, which could indicate fraud. Catching issues early protects your business finances and maintains the integrity of your accounts, offering peace of mind and a clearer picture of your financial health.

Types of bank statements

There are two types of bank statements, paper and digital. Digital bank statements offer several advantages over traditional paper statements, making them a convenient choice for business owners. Digital bank statements are easy to access online, allowing you to view, download, or print them anytime from anywhere. Digital statements also reduce the risk of document loss, as they are stored securely in your online banking portal. By switching to digital bank statements, you can streamline your financial management.

Retrieving bank statements online is simple. Log in to your bank’s website or mobile app, navigate to the statements section, and select the desired time period. Many banks offer search and filter features, making it easier to locate specific transactions.

How electronic statements can save you time and money

By opting for electronic statements, you avoid potential fees associated with mailing and paper processing, which reduces your business expenses. It also reduces paper waste, lowering your environmental footprint. This eco-friendly approach supports sustainability and enhances efficiency, making it a smart choice for modern businesses. In terms of saving time, you can access digital bank statements instantly online, so you don’t have to wait for them to arrive in the mail or organize physical documents. Digital statements also simplify record keeping, as you can quickly search, download, and store them electronically.

Navigating bank fees: What your statements tell you

Bank statements can uncover hidden fees you might not otherwise notice, such as account maintenance charges, ATM fees, or overdraft penalties. When you review your transactions, you can identify these costs and assess whether they are justified or avoidable. To prevent unnecessary fees, consider switching to a bank account with lower or no fees, maintaining minimum balances, or using in-network ATMs. Additionally, set up low-balance alerts to avoid overdraft charges and monitor your account regularly to catch any unexpected charges early.

What is the difference between a bank statement and a transaction history?

A bank statement provides a summarized overview of your account activity over a specific period, typically one month. It shows your starting and ending balances, deposits, withdrawals, and any fees. A transaction history offers a more detailed, real-time record of every individual transaction, such as purchases, transfers, and payments, often without a specified time frame.

Bank statements are ideal when you want to review your overall financial health, to reconcile accounts, and to prepare to file taxes. Transaction histories are useful when you want to track recent activity, to identify errors, or to monitor spending in real time. A regular review of both helps ensure that you address errors promptly and maintain control of your finances.

How bank statements help with filing taxes

Bank statements will help track your business’s progress and, in turn, can serve as a financial record when it comes time to file taxes. While these statements are a record of expenses to your business that include item descriptions and costs, be sure to keep gross receipts and other business documents in order to give a complete picture of your business’s finances when filing your taxes.

There are certain tax forms, such as Form W-2 and Form 1099-MISC, for which bank statements can be especially useful in filing your tax return. In the U.S., the IRS recommends that businesses hold on to their tax returns for at least three years from the time of a tax filing.

Separating your business and personal accounts can help you keep track of the activity related to your business and can help protect your personal accounts. Holding on to your bank statements will not only make tracking business expenses more accessible come tax season, they can also make finding tax deductions associated with those expenses harder to miss.

Understanding tax implications in your bank statements

Bank statements can help with tax reporting in a variety of ways:

- Providing income verification with a statement of deposits and revenue streams

- Identifying expense deductions since many bank statements automatically categorize deductible business expenses, such as supplies, utilities, or travel costs

- Maintaining accurate records with an organized list of transactions to support claims in case of an IRS audit

- Cross-checking financial data with other bookkeeping and payroll records in order to ensure that tax returns are error-free and complete

- Completing tax payments by using transaction history to calculate estimated tax payments throughout the year

- Tracking charitable contributions that may qualify for tax deductions

- Preparing for an audit by providing documented proof of transactions

You can leverage your bank statements to streamline tax reporting tasks, to improve accuracy, and to maintain organized financial records.

Essential for loan applications

When applying for a loan, a lender will typically ask you to include bank statements as a document during the application process. Reviewing your income and cash flow will help a lender determine whether you’re eligible for a business loan. Your bank statement can be used to see how often your business makes deposits, inflows and outflows of cash, and how regularly the account sees activity.

Self-employed individuals and contractors may seek a bank statement loan in lieu of a traditional loan. These loans can be issued based on personal information and bank statements rather than the W-2s, pay stubs, and other employer verification forms a lender may ask of you in a traditional loan application process.

Making the most of your bank statements

Reviewing your bank statements regularly is essential to maintain financial health, to spot errors, and to prevent fraud. By staying vigilant, you can ensure accuracy in your records, avoid unnecessary fees, and make informed decisions for your business. For long-term storage, consider saving digital copies of your bank statements in a secure, cloud-based system or an external hard drive, organized by year or category. Set reminders to review statements monthly and reconcile them with your accounting software to stay on top of your finances. By adopting these habits, you’ll protect your business and build a solid foundation for long-term financial success.

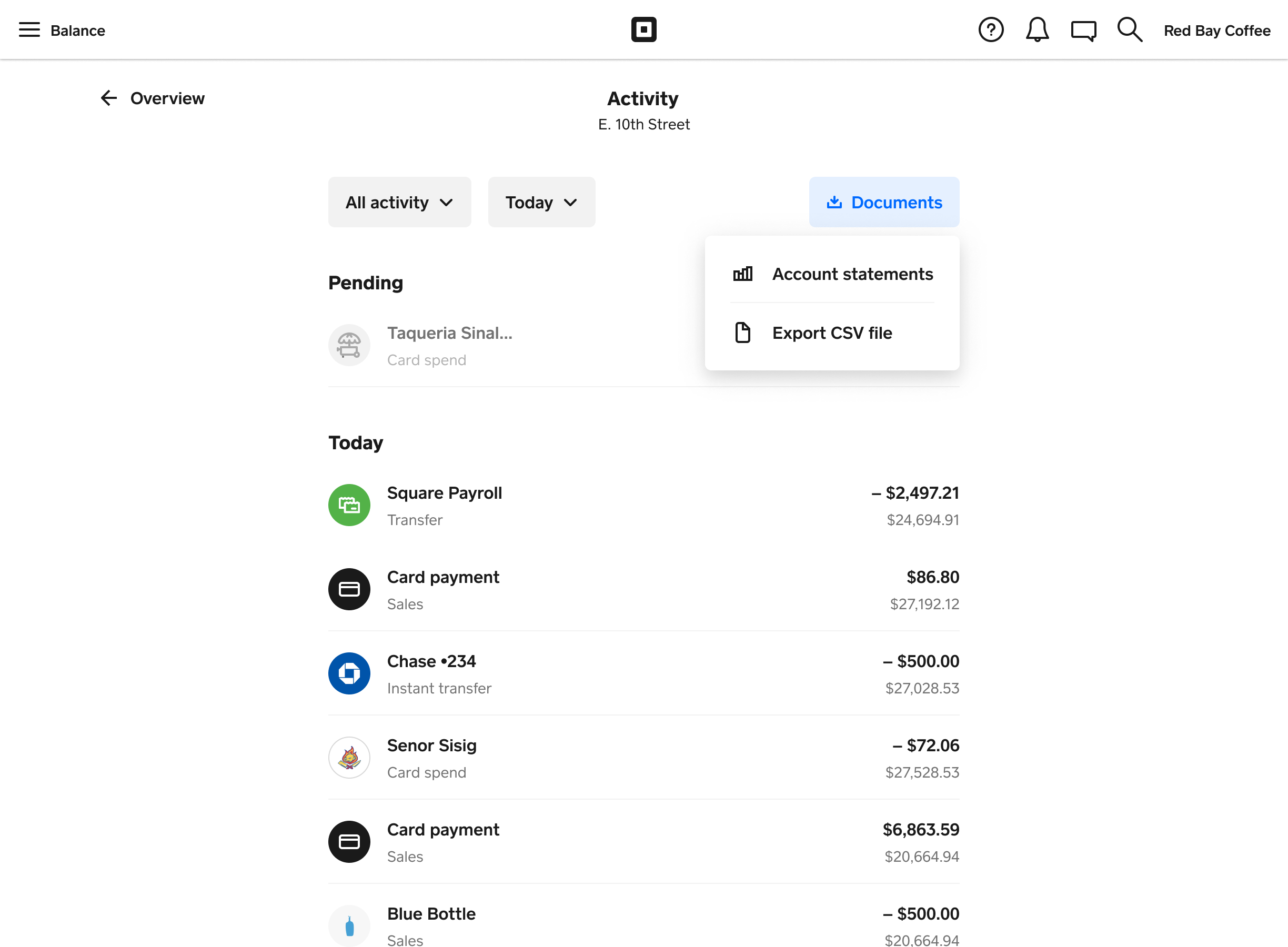

If you’re a Square Banking1 customer, find your Checking statement by navigating to your Square Dashboard and going to Balance > Locations > Checking Settings > Account Statements to download your statement. You can also access your Square bank statements from the Activity page in the documents drop-down menu. Be sure to check your account for the monthly availability of checking and savings statements.]

1. Square, the Square logo, Square Financial Services, Square Capital, and others are trademarks of Block, Inc. and/or its subsidiaries. Square Financial Services, Inc. is a wholly owned subsidiary of Square, Inc.

All loans and Savings accounts are issued by Square Financial Services, Inc., a Utah-Chartered Industrial Bank. Member FDIC. Actual fee depends upon payment card processing history, loan amount and other eligibility factors. A minimum payment of 1/18th of the initial loan balance is required every 60 days and full loan repayment is required within 18 months. Loan eligibility is not guaranteed. All loans are subject to credit approval.

Savings accounts are provided by Square Financial Services, Inc. Member FDIC. Accrue annual percentage yield (APY) of 1.00% per folder on folder balances over $10. APY subject to change, current as of 2/18/2025. No minimum deposit is required to open an account. Accounts will not be charged monthly fees. Accounts are FDIC-insured up to $2,500,000. Pending balances are not subject to FDIC insurance.

Square Checking is provided by Sutton Bank, Member FDIC. Square Debit Card is issued by Sutton Bank, Member FDIC, pursuant to a license from Mastercard International Incorporated, and may be used wherever Mastercard is accepted. Accounts are FDIC-insured up to $250,000. Funds generated through Square’s payment processing services are generally available in the Square checking account balance immediately after a payment is processed. Fund availability times may vary due to technical issues.

![]()