Table of contents

Introduction to Accepting Payments

Getting paid is the bedrock of any business. But if you’re just starting out, the world of payments can be a bit overwhelming. Even if you’ve been around for years, you need to stay current as the payments landscape changes – with card payments and online payments always evolving.

But don’t panic, as this guide walks you through everything you need to know about payment processing and how to accept payments.

What is Payment Processing?

Before you start accepting payments, it’s important to understand what payment processing actually means. In a nutshell, it’s the automatic process which seamlessly moves money from a customer’s bank account to your merchant and business accounts, every time a card transaction is made.

What is a payment processor?

A payment processor is effectively a middleman connecting merchants with customers’ banks. It oversees the transfer of funds whenever an in-store or online card payment is made, by communicating key information between the card itself, the customer’s current account and the company’s bank accounts.

During a transaction, the payment processor checks with a customer’s card network (Visa, for example) and bank to see if they have enough money in their account to cover the sale. If the answer is positive, it relays this information back to the merchant and customer – and allows money to be transferred between their accounts.

What are the fees for processing payments?

The fees your business pays will depend on the agreement you reach with your payment processor. For example, Square bundles up all the different banking and network charges within its card processing fees to make life easier.

The main costs include:

- Payment processor fees. You’ll pay a set fee to your payment processor for each card-present and card-not-present transaction.

- Interchange fees. These are charged by a customer’s bank every time they pay with a card. The card brand, issuer and country of issue can all affect these fees.

- Assessment fees. Card networks like Visa and Mastercard collect these in exchange for processing transactions.

- PCI compliance fees. The costs businesses face to stay compliant with the PCI DSS global card security standard.

How does processing payments work?

The process traditionally follows this route:

- A customer pays by card either in-store or online.

- The merchant’s payment gateway (e.g. a card reader) sends the transaction information to their payment processor.

- The information is then passed to the relevant card network, which in turn gets in touch with the customer’s bank.

- The bank will check if their account has enough money to cover the sale.

- The card network and payment processor are told whether the transaction has been approved or declined – with the latter informing the merchant’s payment gateway of the decision.

- If the sale is approved, funds are transferred from the customer’s account to the company’s merchant account. After a set period, they’re then transferred to the business’s main bank account.

What’s the difference between a payment processor and payment gateway?

The payment gateway is the tool merchants use to accept card payments. In physical stores, they include card-reading devices.

For online stores, they take the form of payment processing portals. The payment gateway is responsible for transferring technical card information from the merchant to their payment processor.

The payment processor is a third party tasked with linking up the different banks and card networks involved in a transaction, once it receives data from the payment gateway. It relays back to the payment gateway whether the transaction has been approved or not.

5 Frequently Asked Questions About Payments

1. How do I accept payments?

To accept payments, you’ll need to get a point-of-sale system (also known as an EPOS). Your POS should be able to handle cash, card payments (especially contactless), mobile payments and even online payments.

2. How are sales deposited?

You’ll need to connect your bank account to your POS. Square’s instant transfer payment schedule is fast and you’ll have the money in your bank account as soon as the next day.

3. What are chargebacks?

Chargebacks happen when customers dispute a charge from your business with their card-issuing bank. When a chargeback occurs, the funds in dispute are held from the merchant while things are worked out.

4. How can I accept contactless card payments?

Contactless card payments are easier and faster to accept than chip and PIN payments. They require a contactless card to be held close to a suitable reader for a payment to complete. In order to accept contactless card payments, you’ll need a reader that does likewise.

5. How can I accept mobile payments?

To accept mobile payments like Apple Pay, Google Pay and Samsung Pay, you’ll need a card reader able to recognise them. To help process payments, customers simply hold their phone to the reader. In the case of Apple Pay, they must also authorise the payment by confirming their face ID.

Choosing a POS to accept payments

To accept payments, you’ll need a point-of-sale (POS) system. A POS contains hardware that allows you to process payments and software that lets you add items and complete a sale. Your EPOS system also takes care of routing funds to your bank account after you make a sale. It’s a key link in the payment processing chain.

When considering a POS to help your business process payments, make sure that it accepts not only cash but also credit card payments and mobile contactless payments (NFC). Since people are increasingly moving away from cash and instead opting to pay with credit cards and digital wallets, it should also be able to link up with online payments.

But your POS system should be able to do a lot more than just process payments. Look for a POS with software that can help run your business from top to bottom (including things like sales reporting, inventory management, employee management and more). Think of your POS as a command centre for your business – not just a hub to accept and process payments. Read our complete guide to POS systems to learn more.

Integrated POS hardware such as a POS register is also a great solution if you’re for those looking for a seamless payment processing experience.

Getting deposits

To receive deposits from sales, you need to connect your POS to your bank account. This is quick and simple with Square. It takes up to seven business days to verify the bank account, and then you’re good to go.

Effectively managing your cash flow can have a massive impact on your business’ success. Look for a system with reliable, fast deposits.

Square’s deposits are reliable – and fast. With our instant transfer payments, funds are deposited in your bank account as soon as the next day. If your business has unique hours, you can also customise the time you’d like transactions grouped for a daily deposit (this is called your “close of day” time).

Managing your receipts

You’ll need to give your customers a record of their transaction (or offer to do so) whenever you accept payments from them. Your POS system should be able to take care of that as well, either through a peripheral paper receipt printer or digital receipts.

Increasingly, businesses and customers are finding digital receipts – those that are emailed or texted – to be the preferred type of payment processing confirmation. Digital receipts save paper and are much more convenient. They’re also a lot easier to keep track of (because let’s be honest, paper receipts often end up in the rubbish).

Receipts have undergone a revolution in the past few years. Digital receipts can now even offer features like customer feedback.

In addition to all the sale details (including taxes, fees or any discounts), your receipts should feature your business’s name and contact information. Square digital receipts (which you can email to people directly after you make a sale) also come packed with other goodies – including a place where customers can quickly send you feedback about their experience.

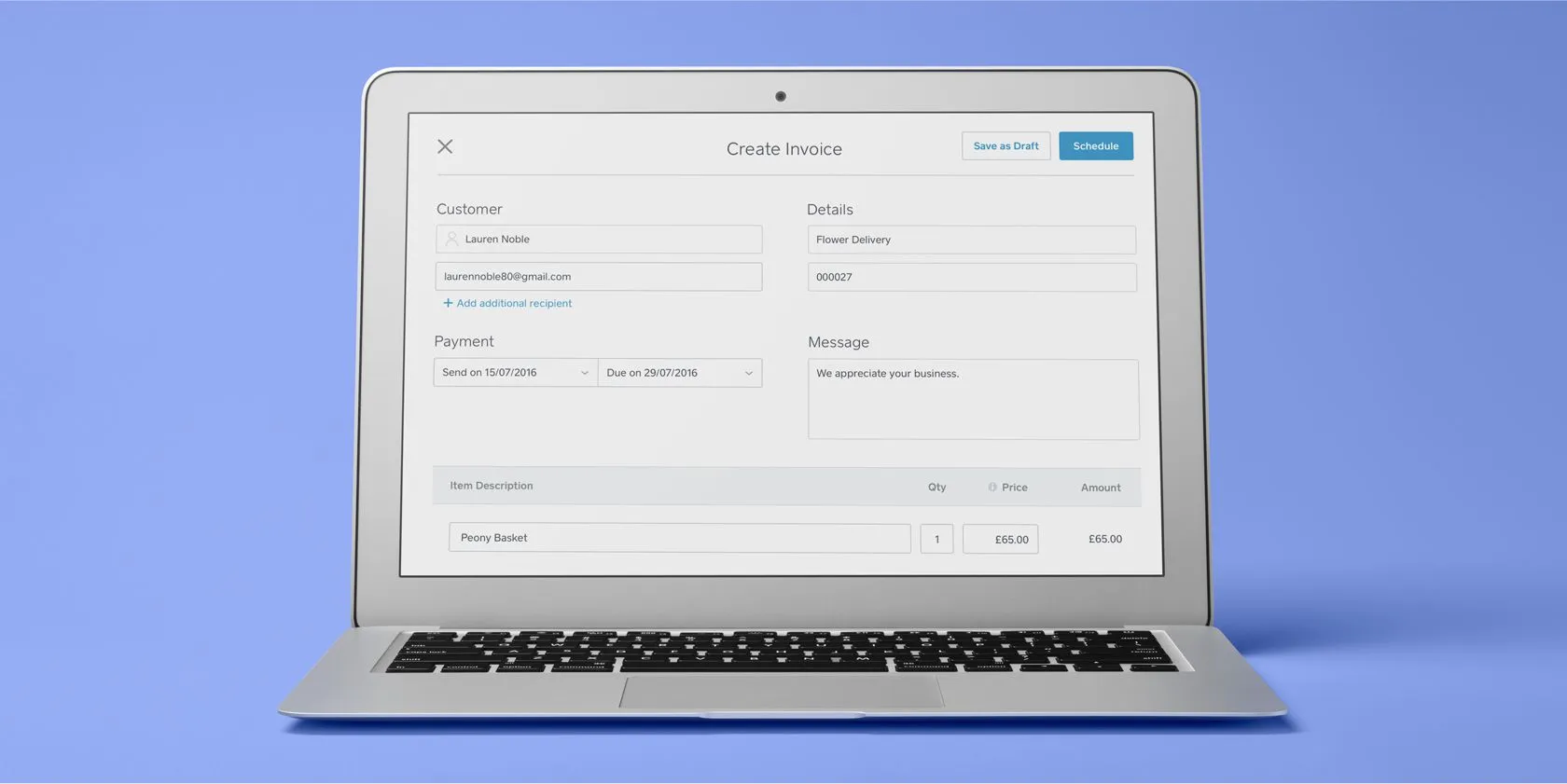

Managing your invoices

If you’re in the services industry, it’s likely you’ll have to create and send invoices to receive and process payments. Just as with receipts, you can opt for paper or digital invoices.

On your invoices, always make sure to include your:

- business information (name, email address, physical address, telephone number);

- customer information (full name and address);

- the invoice number (for your records);

- the date and terms (specifically outlining the time period in which you expect to be paid);

- the price and description of the items (as well as quantity);

- and any taxes, fees and discounts.

Invoices are an extension of your brand and the right templates can help establish a sense of trust and professionalism.

As with receipts, it’s much more streamlined to use digital invoicing. Square offers professional-looking, ready-to-go invoicing templates that you can email out to clients. From there, they can pay you with a click.

You can also keep track of all your invoices in one place in using your Square Dashboard – and sort them by what’s been paid and what’s outstanding.

Managing chargebacks

Chargebacks happen when customers contest a charge on their statement with their card-issuing bank. People contest charges for a number of reasons. Perhaps they don’t recognise the charge or feel the services weren’t up to par with what was advertised.

When there’s a chargeback, the funds in dispute are held from the merchant while the card issuer works things out and decides what to do. “Working things out” can be a complicated, slow and time-consuming process involving a lot of paperwork and documentation. But it’s another potential link to be aware of in the payment processing chain.

Accepting payments from credit cards

If you don’t accept credit cards, it’s likely you’re missing out on sales. Customers are carrying around cash less and less, and the friction of having to find a nearby cashpoint may be enough for them to forgo a purchase. Here are more reasons why it makes sense to accept credit cards at your business:

Payments have gone through several changes—including the shift to contactless cards and the introduction of mobile payments like Apple and Android Pay.

If you don’t accept credit card payments, it’s likely you’re missing out on sales. Customers are carrying around cash less and less, and the friction of having to find a nearby cashpoint may be enough for them to avoid a purchase.

Payments and payment processing services continue to evolve rapidly. Think about how fast the shift to contactless cards, online payments, and the introduction of mobile payments like Apple Pay and Google Pay occurred.

Here are some more reasons why it makes sense to accept credit cards card payments at your business:

You improve your cash flow

Cheques can take a while to clear. Credit card payments, transactions on the other hand, are usually deposited within a few business days.

You bring in more customers

People want convenience from your payment gateway. And if they’re only carrying cards and you don’t accept them, they may skip your business and opt for the competition. Research shows that there were 201 million credit card transactions in February 2021 alone.

Accepting payments from credit cards ensures that your customers have the best experience possible, which makes people more likely to recommend your business to friends.

Your customers spend more

People tend to spend more when they pay with a card. And card spending is growing in a big way – in February 2021, Brits spent £47 billion on debit cards. No longer hindered by the thought of “do I have enough cash on me to cover this?” customers are much freer to spend. That means more impulse buys at the counter.

You instill a sense of trust

If you have stickers or displays near your payment gateway informing customers of all the major cards you accept, that’s likely to instil a sense of trust in people.

You can enjoy safe and secure payments

Credit card payments are heavily screened to reduce the risk of fraud. Square monitors every single transaction so sellers can avoid (major or minor) headaches.

You don’t have to spend much

Even if you’re on a shoestring budget, it’s easy to get set up to accept credit card payments. Square offers affordable credit card readers at a competitive rate of just 1.75% per chip and PIN or contactless payment.

Accepting mobile (NFC) payments

Customers increasingly want to pay ‘contactlessly’ via their mobile devices.

The COVID-19 pandemic is one reason why there’s been a dramatic shift away from chip and PIN transactions towards contactless card and mobile payments. By reducing the need for people to touch card readers, contactless payments tend to be more hygienic.

But contactless payments were growing in popularity even before the pandemic – thanks to their convenience. They’re much faster than chip and PIN transactions as there’s no need to manually type a personal code into the card reader. Mobile payments mean customers don’t need to fumble around trying to remove their cards from their wallets. It’s a quicker process all round for busy shopkeepers and customers on the go.

The UK Government is also making it easier to pay with contactless technology. The limit on contactless payments was raised from £30 to £45 in the spring of 2020. This limit will now be extended even further to £100 in 2021.

Mobile payments require no physical contact between the smartphone and payment gateway – customers just tap or hold their device over the reader to pay. The most popular examples of mobile payment solutions are Apple Pay, Google Pay and Samsung Pay.

It’s important to note these payments are just as secure as chip and PIN. They have several layers of security built into the process to protect banking information. The data involved in a mobile transaction is tokenized and dynamic, so it’s constantly changing. This means the account details on a device can’t be cloned into anything valuable to fraudsters. Combined with 3D Secure, an authentication protocol, these cashless payment methods offer an even higher level of protection against fraud and unauthorised access.

What’s more, Apple Pay is protected by Face ID, Apple’s facial recognition technology. To initiate an Apple Pay transaction, you have to unlock your phone by confirming your facial identity. So even if your device is stolen, no one will be able to get at your data.

Customers can use Apple Pay in your store with a few easy steps:

- After registering their card with their iPhone, they double-click the side button.

- They then authenticate their Face ID by looking at their phone.

- Finally, they place the top of their phone close to your contactless payment reader until a tick and the word ‘Done’ appear.

In contrast to chip and PIN, which can be pretty sluggish, contactless payments are extremely fast (they take just seconds to process). So to provide the best possible customer experience (and future-proof your business), it’s a good idea to be fully equipped to accept both contactless cards and mobile payments.

Square’s suite of point-of-sale hardware can help your business accept and process contactless card and mobile payments with ease. The Square Reader is a portable tool for accepting chip and PIN cards, contactless cards, Apple Pay and Google Pay, while the Square Terminal adds extra functions such as printing receipts.

The Square Register goes even further. It’s a fully integrated point-of-sale system, allowing businesses to manage payments, online sales and deliveries all from one place.

![]()